On-chain OTC, routed by SOR

Traditional OTC desks solve price impact for one trade by moving it off-chain. The cost is fragmentation. Orders sit in private chats and email threads, liquidity is invisible to the broader market and counterparties have to trust each other. C1 Pools take the same idea on-chain. A holder deposits tokens into a C1 Pool at the live oracle price. That deposit is a resting sell order, ask-only, with no curve and no slippage. Every DEX aggregator that has indexed FlowState sees that liquidity in their SOR. When a buyer submits a trade through any of those aggregators, the router compares net execution prices and matches the buyer into the C1 Pool because it is mathematically the cheapest source. The seller gets OTC-quality execution. The buyer gets aggregator-native routing. The trade settles on-chain at oracle price. Liquidity stays visible, composable and on-chain.Why oracle pricing eliminates price impact

The AMM model has one fundamental limitation: it must derive price from internal pool state. The ratio of reserves sets the price. When the ratio changes (because someone trades), the price changes. This is unavoidable under the constant product formula. C1 Pools invert this. Price is set by an external oracle (Pyth or Chainlink), not by pool state. The pool does not need to rebalance because it does not set the price. The price comes from the market. This eliminates price impact at the source, not as a workaround.

Oracle-priced settlement vs AMM bonding curve

How a C1 Pool works

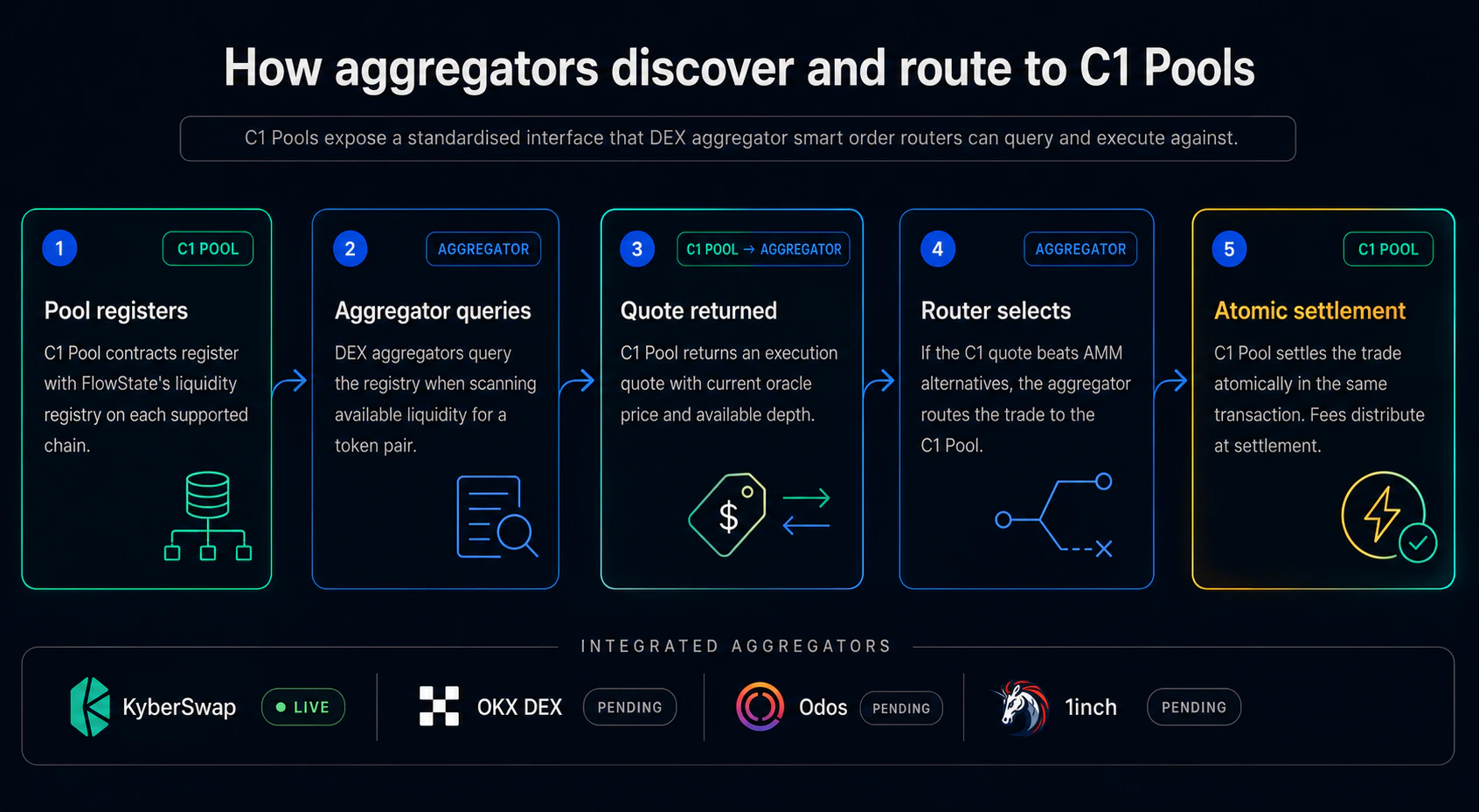

1

A holder deposits tokens

Any token holder (a VC, a project treasury, a team member unlocking vested tokens) deposits their tokens into a C1 Pool. The pool accepts single-sided deposits. No need to pair with ETH or a stablecoin. Deposited tokens are priced at the live oracle market rate. No discount, no vesting delay, no bonding curve.

2

DEX aggregators discover the pool

C1 Pools are registered as liquidity sources with major DEX aggregators. KyberSwap is live. OKX DEX, Odos and 1inch are in integration. Smart order routers scan all available liquidity sources simultaneously when a buyer submits a trade: AMM pools (V2, V3, V4), order books, RFQ sources and C1 Pools.

3

The router selects C1 first

For any trade involving a token with C1 liquidity available, the oracle-priced pool offers a better execution price than the AMM alternative. The AMM curve forces each additional token to cost more. C1 Pools price every token at market. Smart order routers select C1 first whenever C1 liquidity is available, because it is the best-execution path by every metric the router optimises against. This is not a commercial negotiation. It is the output of the router’s price comparison logic.

4

The buyer receives tokens at market price

Settlement is instant. No vesting, no bonding curves, no delays. The buyer receives exactly what they expect at exactly the price they quoted.

5

The seller receives market proceeds minus 1% fee

The depositing holder receives settlement in the base currency (USDC or ETH) at the oracle price, minus the 1% protocol fee. Even after the fee, they receive substantially more than any AMM exit would yield on a position of comparable size.

Why routers always prioritise C1

This is the structural engine that drives adoption without requiring direct user acquisition. When a DEX aggregator evaluates liquidity sources for a given trade, it compares the net execution price across every available option, including fees and slippage. For a $100K trade on a token with $2M AMM liquidity, the comparison looks like this:

How smart order routers select C1 Pools

What makes C1 Pools structurally different

Single-sided deposits

Traditional AMM LPs must deposit two assets in equal value. C1 Pools accept only the token being sold. This removes the primary barrier for large holders: they hold the asset, they do not need to acquire a pair asset to provide liquidity.

Oracle-priced execution

Price is set by Pyth or Chainlink oracle feeds, not internal pool state. No curve. No rebalancing. No impermanent loss for depositors. The price the buyer sees is the same price as any CEX.

Aggregator-native routing

C1 Pools plug directly into the smart order routing infrastructure that already exists. Buyers do not need to know FlowState exists. They get C1 execution when using their existing aggregator of choice.

Holder-sourced liquidity

The market’s liquidity providers are the trapped holders themselves. FlowState does not need to bootstrap a professional market maker ecosystem. The pain point and the solution are aligned in the same party.

C1 Pool coverage is bounded by oracle availability. Pyth and Chainlink together cover thousands of tokens, but the long tail of tokens without oracle feeds cannot be served by C1. For tokens outside oracle coverage, AMM remains the only option. Oracle expansion is an active part of the roadmap.

C1 Pools vs AMM liquidity

A new liquidity primitive

AMMs are permissionless and flexible but curve-bound. Order books are efficient and slippage-free but centralised. OTC desks are zero-impact but off-chain and fragmented. C1 Pools are permissionless, on-chain, zero price impact and always best-priced. C1 Pools do not replace AMMs. They upgrade the market. Aggregators continue routing through AMMs when C1 liquidity is not available. But for every token where a holder has deposited into a C1 Pool, that token has a better execution option, and the router uses it automatically.Next: The Fee Model

Why a 1% fee is one of the highest in DeFi and the buyer still gets the best execution available.