How AMMs price trades

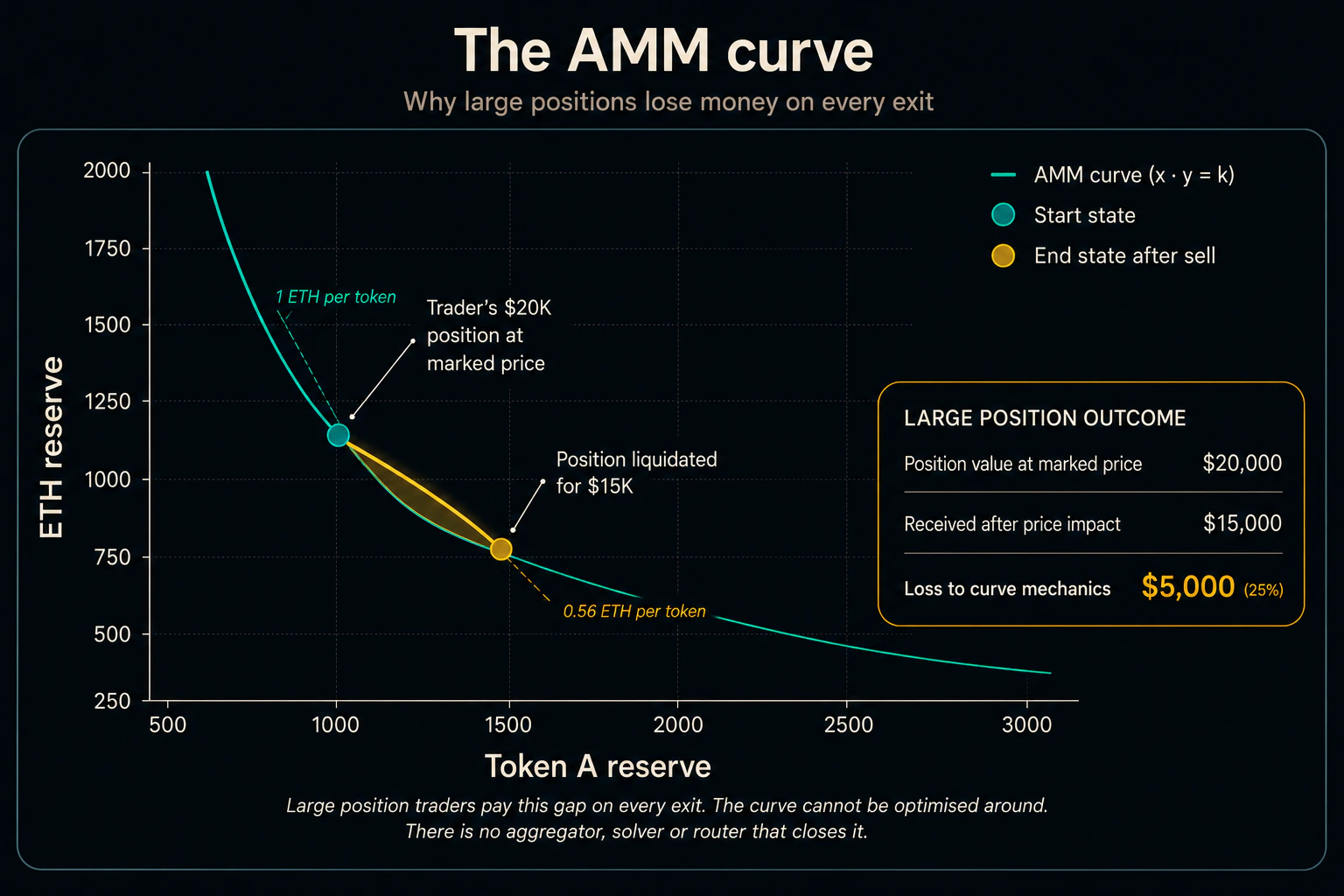

Uniswap and similar AMMs use the constant product formula (x · y = k) to price every trade against pool reserves. As a buyer purchases tokens, the pool’s reserve ratio shifts, and the price moves up the curve. Larger trades move the price further. This is the AMM’s pricing mechanism, not a flaw in it. The result is price impact: the cost of moving the curve. It exists on every AMM trade. For deeply liquid pairs (ETH/USDC, BTC/USDT), the impact is small. For thin-liquidity tokens, it is catastrophic.

The constant product curve: every additional token costs more than the last

Why existing solutions don’t cover this segment

DeFi has produced sophisticated liquidity models over the past five years: AMMs and concentrated liquidity, intent systems, PMM platforms, prop AMMs and on-chain orderbooks. Each is engineered for a specific segment and serves that segment well. None reach thin liquidity tokens because the economic assumptions that make those models work in their target segment do not hold here. Solvers need hedging venues, PMMs need CEX markets, prop AMMs need CEX price feeds, orderbooks need active market makers and concentrated liquidity is still curve-bound. C1 Pools sit alongside this stack as the layer those models cannot reach: oracle-priced, single-sided, sourced directly from holders. The FlowState vs Other Liquidity Models page covers each model in detail.Where price impact gets catastrophic

Roughly 95% of actively traded tokens sit below $5M in liquidity. A token with a $178M market cap and $2.9M in liquidity (a real-world example) cannot absorb a 1% supply exit without the seller losing more than half the position’s stated value.

Why large holders cannot exit

Early VCs, project treasuries, team allocations and market participants holding 1-10% of a token’s supply face the same wall. Their positions exist on paper but cannot be liquidated at fair value. Estimated total stock of trapped positions across small and mid-cap tokens runs $50-100B. This is separate from the annual flow of value destroyed to slippage on trades that do execute, addressed in the next section. This is normal market mechanics, not a market crash. The pool is physically unable to absorb the trade.Why existing solutions don’t cover this segment

Intent systems (UniswapX, CoW Protocol, 1inch Fusion+)

Intent systems (UniswapX, CoW Protocol, 1inch Fusion+)

Solvers fill orders for pairs they can profitably hedge. Thin-liquidity tokens have no hedging venue. The top three UniswapX fillers hold 79% of daily volume and trade exclusively in liquid pairs. CoW reached 34.3% of DEX aggregation share in July 2025, but its Coincidence of Wants requires opposite orders to exist simultaneously, which long-tail tokens lack.

RFQ and PMM platforms (Hashflow, Bebop)

RFQ and PMM platforms (Hashflow, Bebop)

Professional market makers quote on assets they can hedge on a CEX. Thin-liquidity tokens are not on any CEX and have no derivatives market. Industry standard capital requirements for professional market making run $1-10M per venue. Bebop’s PMM coverage is approximately 50 tokens. Hashflow’s documentation explicitly acknowledges that non-PMM tokens route through standard AMMs.

Prop AMMs (HumidiFi, Lifinity)

Prop AMMs (HumidiFi, Lifinity)

Validated oracle pricing at scale. HumidiFi processed 150B cumulative volume because faster oracle updates won the liquid-pair segment. Validated oracle pricing at scale. HumidiFi processed $100B cumulative volume in five months on Solana. But Prop AMMs require off-chain CEX price feeds. Thin-liquidity tokens discover price on-chain only, making oracle-based models circular. Lifinity shut down in December 2025 after $150B cumulative volume because faster oracle updates won the liquid-pair segment.

Concentrated liquidity (Uniswap V3, Arrakis)

Concentrated liquidity (Uniswap V3, Arrakis)

Improves capital efficiency within the AMM model, does not escape it. Large trades exhaust nearby liquidity and cross into lower-depth ticks, delivering the same slippage as V2 pools at larger sizes. Over 51% of V3 LPs were unprofitable because impermanent loss exceeded fees, discouraging the deep provisioning that would be needed to serve large trades.

The size of the gap

Approximately $366B of annual volume trades through tokens with sub-$5M liquidity. At a weighted average loss of 13.8% to price impact, that is $25-50B in annual flow destroyed by curve mechanics. This is annual realised loss on trades that do execute, separate from the $50-100B stock of trapped positions that cannot exit at all. None of it goes to LPs. None of it goes to protocols. It is pure inefficiency. This is the segment FlowState serves. The next page explains how.Next: C1 Pools Explained

How oracle-priced, single-sided liquidity eliminates price impact at the architectural level.